Securing Debit Orders with Halo Dot

DebiCheck is a payment authentication system that was implemented to enhance security and reduce fraud in the South African banking industry. While this is called DebiCheck in South Africa, many countries worldwide have their own form of Debit Order Authentication under a different name.

In the last several years, there has been an increase in fraudulent debit orders being processed without permission from consumers in South Africa. There was also an increase in consumers disputing debit orders that were in fact valid. As a result, the South African Reserve Bank (SARB) introduced DebiCheck as a mandatory system to protect consumers and improve the overall integrity of the payment system.

DebiCheck is a verification process that ensures that debit orders are authorised by the account holders before they are processed. This system aims to protect consumer from unauthorised debit orders and provide businesses with a reliable and efficient payment collection method (PASA).

The main goals of implementing DebiCheck were:

- To enhance security

- To reduce fraud

- To improve transparency in the payment process

By verifying the authenticity of debit order mandates, the system ensures that customers have full control over their accounts and can prevent unauthorised transactions.

Before DebiCheck

Before DebiCheck, AEDO and NAEDO were two standards that worked together to process debit orders in South Africa.

AEDO

AEDO stands for Authenticated Early Debit Order, which required a physical mandate to be authenticated using the customer’s bankcard and PIN.

This system was designed to give creditors a higher likelihood of successful connections as debits were processed early in the morning with the hopes that funds were available in the customer’s account. The requirement for the customer to authenticate the debit order with their bank card and PIN offered higher security as it was more difficult for unauthorised debit orders to be processed.

NAEDO

NAEDO stands for Non-Authenticated Early Debit Order which allowed for non-authenticated mandates, meaning that a debit order could be processed based on a signed mandate without real-time authentication.

NAEDO transactions had a lower priority compared to AEDO transactions but still benefitted from early processing. Real-time authentication wasn’t a requirement for NAEDO transactions which led to issues of higher incidence of unauthorised debit orders, disputes and fraud.

DebiCheck was introduced as it combined the early processing benefits of AEDO and NAEDO with real time electronic mandate confirmation, ensuring that all debit orders were authenticated directly with the consumers bank before processing. This addressed the vulnerabilities of NAEDO while maintaining the high security of AEDO.

How DebiCheck Traditionally Works

DebiCheck works by requiring account holders to authenticate their debit order mandates through a verification process.

- Your bank will send you a request to confirm the new DebiCheck payment information. Approval or authorisation can be given in several ways – like using your banking app, your card and your PIN (available in branch/using an ATM/POS machine only), or through internet banking.

- Once you confirm that the information is correct, your bank will load the information on a mandate register and send a confirmation message to your service or credit provider.

- Every time that the debit order is processed to your account, your bank must first verify that the debit order information is correct against the information on the DebiCheck register.

- DebiCheck collections are only processed if the critical information matches. If it does not match, the DebiCheck collection is rejected.

Through this process, both the consumer and the merchant agree to the same debit order terms and to the debit order being loaded.

Key Benefits of DebiCheck for Businesses and Consumers

DebiCheck offers several key benefits for both consumers and businesses:

- Enhanced Security – DebiCheck provides an additional layer of security by verifying the authenticity of debit order mandates, reducing the risk for fraudulent transactions.

- Consumer Protection – The system ensures that consumers have control over their bank accounts and can prevent unauthorised debit orders, protecting them from financial losses.

- Efficient Payment Collection – Businesses benefit as it provides a reliable and efficient method for collecting payments. By ensuring that debit orders are authorised, businesses can reduce the number of failed payments and improve cash flow.

- Reduced Disputes – The likelihood of disputes between businesses and consumers regarding unauthorised debit orders is minimised, resulting in smoother transactions and fewer customer complaints.

Different forms of DebiCheck Authentication Mechanisms

DebiCheck mandates can be authenticated through various different methods, categorised as TT1, TT2 and TT3.

TT1 Authentication - Real Time

An immediate message is sent to the bank account holder allowing for instant mandate authentication.

- Processing time: Real Time.

- Timeframe to Respond: 120 Seconds

- Authentication Channels: Banking app; Online Banking; USSD; Branch; Contact Centre

TT1 Authentication - Batch

A delayed message is sent to the bank account holder allowing for authentication.

- Processing Time: Batch

- Timeframe to Respond: Same Day

- Authentication Channels: Banking App; Online Banking; USSD; Branch; Contact Centre

TT2 Authentication

Authentication requests are batched and sent to all prospective clients at the same time. The response is received within two days.

- Processing Time: Batch

- Timeframe to Respond: Within 48 hours

- Authentication Channels: Banking App; Online Banking; USSD; Branch; Contact Centre

TT3 Authentication

This is a form of upfront authentication, requiring a face-to-face interaction whereby the debtor needs to swipe, insert or tap their card on a POS machine. The authentication is in real time and requires no further action from the debtor.

- Processing Time: Real Time

- Timeframe to Respond: Immediate

- Authentication Channels: POS; ATM

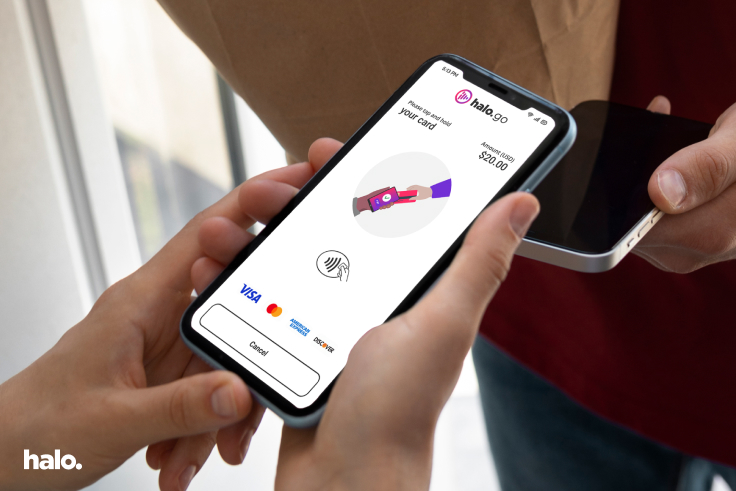

Halo Dot and DebiCheck

At Halo Dot, we offer the possibility to authenticate your DebiCheck Mandates using the TT3 authentication mechanism. TT3 is card based authentication that can be done in real time, either on an ATM or a POS device.

Traditionally, people associate SoftPOS with only payment acceptance. TT3 is a feature that can be consumed by any of our products. As our software turns your mobile device into a POS terminal, you will be able to authenticate a DebiCheck transaction on that very device.

This benefits the consumer as they need to take no further action. This benefits the merchant as they are able to put a device in their agent/brokers hands at a fraction of the cost and there is a reduced drop off rate where consumers fail to authenticate their debit orders at a later time. This is a great use case that we’re exploring with several insurance agencies in South Africa, empowering their agents in the field to load and authenticate debit orders easily. Any company that accepts debit orders as a form of recurring payment acceptance can benefit from this solution.

Reach out to Halo Dot today to find out more about our debit order authentication solutions and how you can implement this system in your business today.